This recalibration of our policy stance will help maintain the strength of the economy and the labor market…

– Federal Reserve Chairman Jerome Powell

Ongoing economic growth, improving inflation, and the first of what is likely to be multiple, periodic rate reductions by the Federal Reserve all fueled yet another quarterly advance for U.S. equities, the seventh advance in the last eight quarters. As investors anticipate moderately lower interest rates going into and through 2025, their appetite broadened beyond the small cadre of technology stocks that have driven performance for the last 18 months.

Ongoing economic growth, improving inflation, and the first of what is likely to be multiple, periodic rate reductions by the Federal Reserve all fueled yet another quarterly advance for U.S. equities, the seventh advance in the last eight quarters. As investors anticipate moderately lower interest rates going into and through 2025, their appetite broadened beyond the small cadre of technology stocks that have driven performance for the last 18 months.

Investors can hardly be faulted for their optimism. The U.S. labor market remains strong, consumer spending has been resilient, inflation continues to improve, lower interest rates should relieve some stress among lower income households with debt and add some lubricant to the real estate market, where higher mortgage rates have dampened activity and priced many would-be home buyers out of the market. Economically speaking, the U.S. continues to perform well, and certainly better than most of the rest of the world.

With that said, on October 1, east and gulf coast dockworkers went on strike, a development that, if it drags on more than a few weeks, will dampen economic activity at some point during the fourth quarter. Moreover, the upcoming election will have important implications for overall economic activity, and while those economic implications won’t become reality until 2025, investor anticipation will manifest itself in financial markets during the fourth quarter. As such, we see the upcoming election as the most pertinent risk investors must confront as we close out 2024 and look to the next president’s term, especially when it comes to the sectors and companies most impacted, positively and negatively, by the next presidential administration.

The Global Economy

Global economic activity slowed somewhat during the quarter but remains moderately positive overall. Favorable labor markets support consumer spending while inflation continues to improve, allowing central banks to lower their benchmark rates and provide some support to economic activity.

Global economic activity slowed somewhat during the quarter but remains moderately positive overall. Favorable labor markets support consumer spending while inflation continues to improve, allowing central banks to lower their benchmark rates and provide some support to economic activity.

The path to lower rates isn’t clear for every economy, however. In Europe, economic activity is stagnating, but inflation remains too high for some of the more inflation-focused hawks on the European Central Bank to support aggressive rate reductions. That economy may need to experience some additional weakness before inflation settles into a level that opens the door for meaningful monetary policy support.

In the U.S., third quarter economic activity looked a lot like it has for the past few quarters; a well-balanced labor market underpinning moderate consumer spending. With inflation moving lower, the Federal Reserve felt confident enough to lower its benchmark rate 0.50% in September, initiating what is likely to be a multi-year recalibration process.

At 0.50%, its initial move is double the size of its typical adjustment (0.25%), but one that, in our opinion, makes sense. Rather than signaling concern about economic strength overall, the Federal Reserve is signaling that it understands the plight of lower-income households, and that it wants to provide support quickly. With inflation trending lower, it has the luxury of starting with a larger move to front-load some of the benefits, which are already starting to work their way through the financial system to borrowers and would-be home buyers in the form of lower credit card, loan, and mortgage rates and to investors in the form of higher equity and bond prices.

Equities

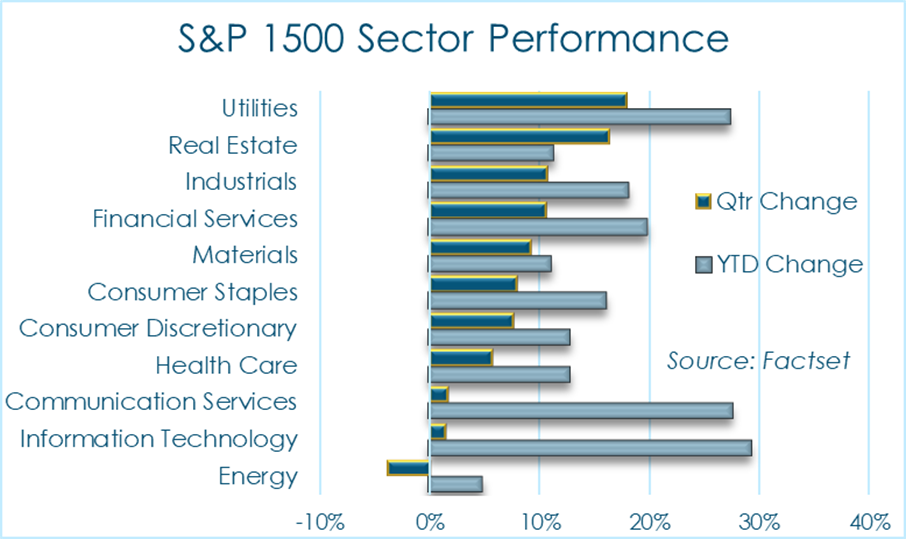

U.S. equity markets turned in another quarterly advance, but unlike many of the previous quarters, this quarter’s leaders fall outside the Information Technology sector. The Federal Reserve’s initial rate reduction sparked renewed enthusiasm for interest-rate sensitive sectors such as Utilities and Real Estate. Information Technology and Communications Services remain year to date leaders, but broad-based strength across most sectors suggests investors appreciate the Federal Reserve’s willingness to remove some of its restraint and support economic activity.

U.S. equity markets turned in another quarterly advance, but unlike many of the previous quarters, this quarter’s leaders fall outside the Information Technology sector. The Federal Reserve’s initial rate reduction sparked renewed enthusiasm for interest-rate sensitive sectors such as Utilities and Real Estate. Information Technology and Communications Services remain year to date leaders, but broad-based strength across most sectors suggests investors appreciate the Federal Reserve’s willingness to remove some of its restraint and support economic activity.

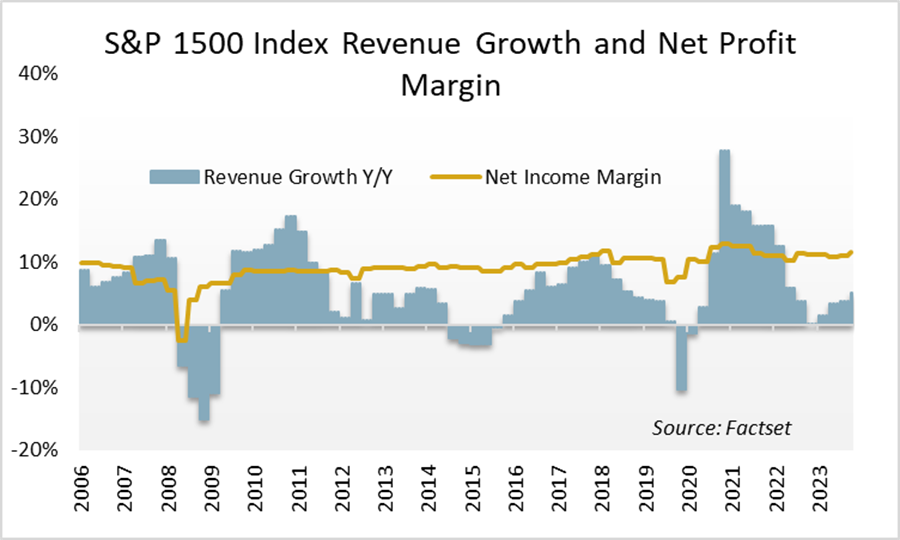

Broad based strength also reflects investor appreciation for corporate execution during recent challenging and dynamic business environments. Second quarter earnings, reported during the third quarter, held up well, and the outlook for earnings the remainder of this year and next are positive. We attribute this largely to management teams’ ability to maintain profit margins despite dramatically slowing revenue growth. As revenue growth rebounds, the opportunity to deliver upper-single digit or even low

Broad based strength also reflects investor appreciation for corporate execution during recent challenging and dynamic business environments. Second quarter earnings, reported during the third quarter, held up well, and the outlook for earnings the remainder of this year and next are positive. We attribute this largely to management teams’ ability to maintain profit margins despite dramatically slowing revenue growth. As revenue growth rebounds, the opportunity to deliver upper-single digit or even low  double-digit earnings growth becomes more plausible.

double-digit earnings growth becomes more plausible.

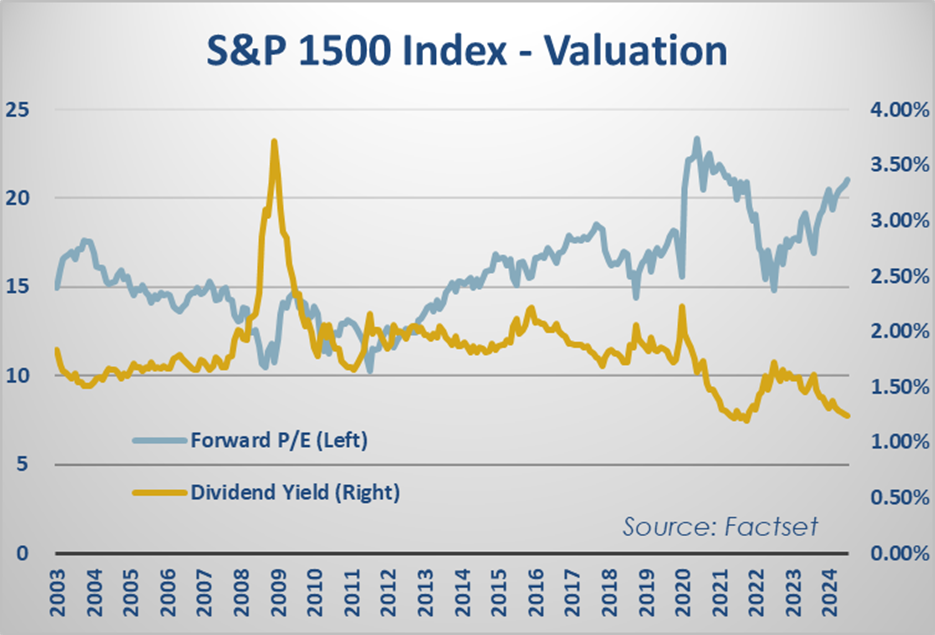

Which is in fact what investors expect for 2025, reflected in both earnings estimates and the ongoing climb in the Price / Earnings ratio. Using this metric, stocks would appear to be as richly valued as at any time during the last 20 years. However, using our preferred metric, inflation-adjusted Free Cash Flow Yield, stocks appear to be less expensive than their five-year average, and only somewhat more expensive than their 15-year average. As such, given the economic backdrop, we’re not overly concerned about equity valuations overall, at least not as a catalyst for a potential equity market correction.

Fixed Income

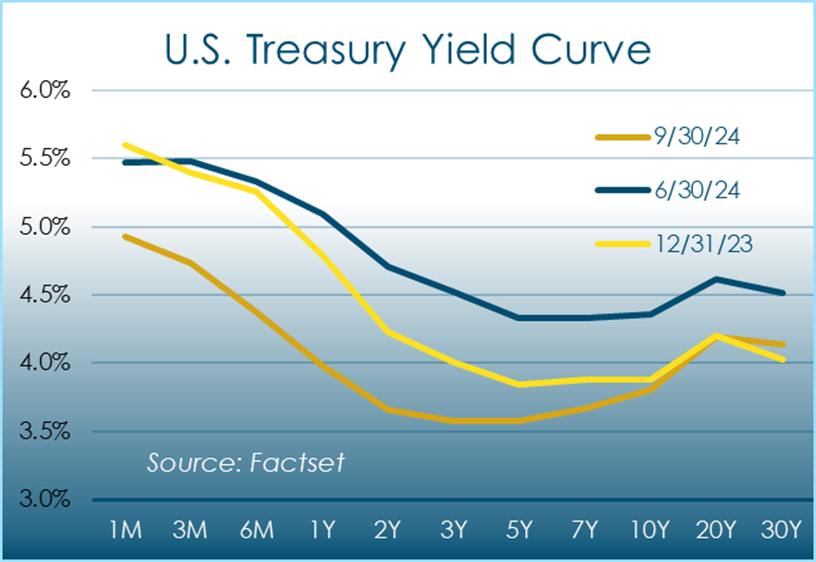

Bond investors also cheered the Federal Reserve’s decision in September, although they had been anticipating it for most of the quarter. With inflation subsiding and the labor market settling into a better balance, rates on U.S. Treasuries declined over the quarter, bringing the widely watched 2-year vs 10-year yield differential back into positive territory for the first time since July 2022.

Bond investors also cheered the Federal Reserve’s decision in September, although they had been anticipating it for most of the quarter. With inflation subsiding and the labor market settling into a better balance, rates on U.S. Treasuries declined over the quarter, bringing the widely watched 2-year vs 10-year yield differential back into positive territory for the first time since July 2022.

Typically, declining yields on 10-year Treasuries would signal deteriorating economic conditions, however, in this case, we believe it signals investor confidence that inflation will moderate further, allowing the Federal Reserve to continue to lower its benchmark rate, ultimately bottoming out around 3% and remaining there for a number of years, assuming the economy settles into a moderate, but steady pace of growth and modest pace of inflation.

Commodities

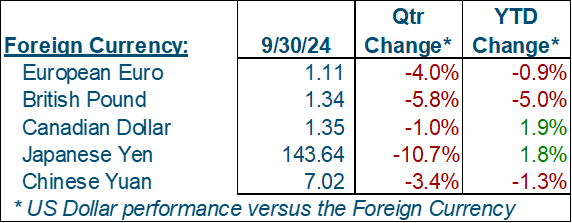

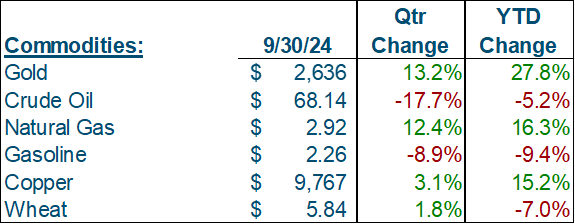

Within the commodity complex, gold had another strong quarter, propelling its year-to-date performance past U.S. Equities. Falling interest rates, moderating inflation, and a weaker U.S. dollar are all supportive for gold prices.

Within the commodity complex, gold had another strong quarter, propelling its year-to-date performance past U.S. Equities. Falling interest rates, moderating inflation, and a weaker U.S. dollar are all supportive for gold prices.

Conclusion

Clearly the economic backdrop is conducive to positive financial market performance, and Federal Reserve actions are likely to lend even more tailwinds to the economy and financial markets. With that said, investors will have to confront three distinct risks during the remainder of 2024, two of which are likely to persist well into 2025.

Abroad, Israel’s direct actions against Hezbollah and its leaders, some of which it has taken on Iranian soil, amplify the unpredictability of the conflict, something investors will struggle to quantify let alone mitigate. In the U.S., labor strikes at east coast and gulf coast ports will constrain imports, and though shippers have been expediting deliveries in anticipation of a strike, goods that aren’t already offloaded may not make it onto store shelves in time for the holiday shopping season. Given the ILA’s terms (77% pay raises over 6 years, among other things), it’s hard to see how the strike will be resolved quickly without government intervention, something we see as unlikely prior to the presidential election.

Which is, in fact, the biggest risk we see for investors moving into 2025. Both candidates have adopted unorthodox economic platforms widely derided among historians and economists. However, because many of their policies can be enacted without congressional approval, they pose material risks for the overall economy, and in particular, specific sectors and companies.

For example, Trump’s promise to implement universal tariffs on all imports, would, if enacted as promised, lead to an immediate inflationary spike in the price of goods, to which the Federal Reserve would have to respond forcefully, resulting in significantly higher interest rates, significantly diminished household wealth, and almost certainly a recession. We find it puzzling that he would cite McKinley and his disastrous tariff policies as an economic role model when virtually every historian and economist associates him and his policies with recession and household wealth destruction. If Trump is in fact using them as a negotiating tactic to gain leverage with trading partners, as he successfully did during his first term, then their impact won’t be as universally negative because importers will find ways around them by importing goods from preferred countries, and U.S. exporters will gain new or expanded access to foreign markets currently protected by other nations’ trade-protectionist policies. Nevertheless, the cult of McKinley within the Republican party is real and so Trump’s threats to employ tariffs are too potentially devastating for investors to ignore.

Harris on the other hand is less focused on trade and more focused on using regulations and regulatory agencies to remake the U.S. economy from the inside. Ironically, the vast majority of studies evaluating the economic impact of regulations conclude that government regulations are just as, if not more, pernicious to the American economy than tariffs. Her baseless accusations that grocery stores are price gouging consumers is just one warning signal to investors that a Harris administration would, perhaps out of ignorance, perhaps out of political motivation, target random sectors and companies with regulations and Department of Justice investigations in order to realize her vision for the U.S.

In a regrettable turn of events, these are the two candidates U.S. voters must choose from to lead this country for the next four years. Although Trump’s policies may ultimately be less deleterious than Harris’, both candidates’ rhetoric and ultimate implementation will be unpredictable and at the same time, monumentally important for the decisions companies make (like hiring employees or investing capital) and the results they ultimately deliver for investors.

Which is why we view the upcoming election as the single most important risk factor investors must confront as we conclude 2024 and look forward to 2025 and beyond. The Federal Reserve has done a remarkable job guiding the U.S. economy into a sustainable, steady pace of growth characterized by a strong but balanced labor market and moderate inflation. We just hope, perhaps in vain, that our next president doesn’t squander it.