I try to learn from the past, but I plan for the future

by focusing exclusively on the present. – Donald Trump

U.S. equities concluded 2024 with yet another advance, delivering positive results for the eighth quarter out of the last nine. The AI fervor that began in the spring of 2023 continues to propel broader markets higher, especially the tech-centric Nasdaq index.

U.S. equities concluded 2024 with yet another advance, delivering positive results for the eighth quarter out of the last nine. The AI fervor that began in the spring of 2023 continues to propel broader markets higher, especially the tech-centric Nasdaq index.

The supportive backdrop that existed during the third quarter, namely steady economic growth, improving inflation, and the Federal Reserve’s policy recalibration, continue to support equity prices. But in November, equity markets got another pillar of support when it became clear that Donald Trump would become the 47th President of the United States, and that he would have a (narrow) Republican majority in both chambers of Congress.

In our third quarter 2024 Review, we voiced our concerns about Trump’s trade policies, somewhat perplexed that he would cite former president McKinley’s disastrous trade policies as a model for the U.S. going forward. Investors seem to be less concerned; virtually all of the fourth quarter’s equity market gains occurred after November 5. Perhaps more importantly however, small businesses resoundingly welcomed the election result and because of it, are much more enthusiastic about the direction of the U.S. economy; as they make capital outlays and expand their employee base, they will add further support to an economy already on solid footing.

So, despite our misgivings about his potential trade-related policies, business and investor confidence are important tailwinds that should support respectable economic growth and equity market performance during 2025 and beyond. As such, our constructive outlook persists, for the U.S. economy and equity markets. With back-to-back years of 25% returns, an equity market correction is a virtual certainty, but the multi-year upward trend should remain intact in 2025.

The Global Economy

Global economic growth was positive during the fourth quarter, but the dispersion between developed economies and emerging economies is growing. Outside the U.S., developed economies are struggling to post inflation-adjusted growth above 1% while emerging economies, where demographic growth is stronger, continue to post economic growth rates in the mid-single digits.

Global economic growth was positive during the fourth quarter, but the dispersion between developed economies and emerging economies is growing. Outside the U.S., developed economies are struggling to post inflation-adjusted growth above 1% while emerging economies, where demographic growth is stronger, continue to post economic growth rates in the mid-single digits.

The global manufacturing sector continues to struggle, especially in developed economies where consumers continue to prefer services over goods. Central banks are stuck in no-man’s land, eager to provide more support for fragile economies, but wary that doing so could blunt, or even reverse, recent improvements on the inflation front. Unfortunately, clear evidence that inflation has resumed its downward trend may only occur as a result of further economic weakness.

In the U.S., economic growth continues to be best in class among developed nations. In fact, the U.S. economy exits 2024 in what could almost be described as a goldilocks scenario. A strong labor market, healthy consumer, and now, a business-friendly political climate all suggest that U.S. economic outperformance should continue into 2025. The only blemish, in our opinion, is the stubbornness of inflation, which, as we’ve discussed previously, asymmetrically strains lower income households.

Which is why the Federal Reserve signaled in December that it expects to reduce its benchmark interest rate only 0.5% in 2025, half of what it expected when it met in September. The Fed governors’ left-leaning political bias is unquestionable, and so, right-leaning politicians may jadedly ascribe the Fed’s slower pace of rate reductions to its reluctance to do anything that helps Trump and his fellow Republicans. However, in this case, because inflation’s improvement has slowed, the “last mile” of additional improvement is not a given. Moreover, Trump’s trade policies, if enacted in the extreme, would be inflationary, so the Fed’s wait and see approach seems reasonable in our opinion. Investors, for their part, don’t appear to be overly concerned about the slower pace of rate reductions, focusing instead on his pro-business policies as an incremental tailwind for equities going into 2025.

Equities

Although positive U.S. equity performance during the fourth quarter came exclusively after November 5, and as a result, it would be easy to ascribe the fourth quarter’s performance entirely to Trump and his fellow Republicans’ victory, in reality, the fourth quarter’s advance was simply an extension of the strength that persisted all year.

Although positive U.S. equity performance during the fourth quarter came exclusively after November 5, and as a result, it would be easy to ascribe the fourth quarter’s performance entirely to Trump and his fellow Republicans’ victory, in reality, the fourth quarter’s advance was simply an extension of the strength that persisted all year.

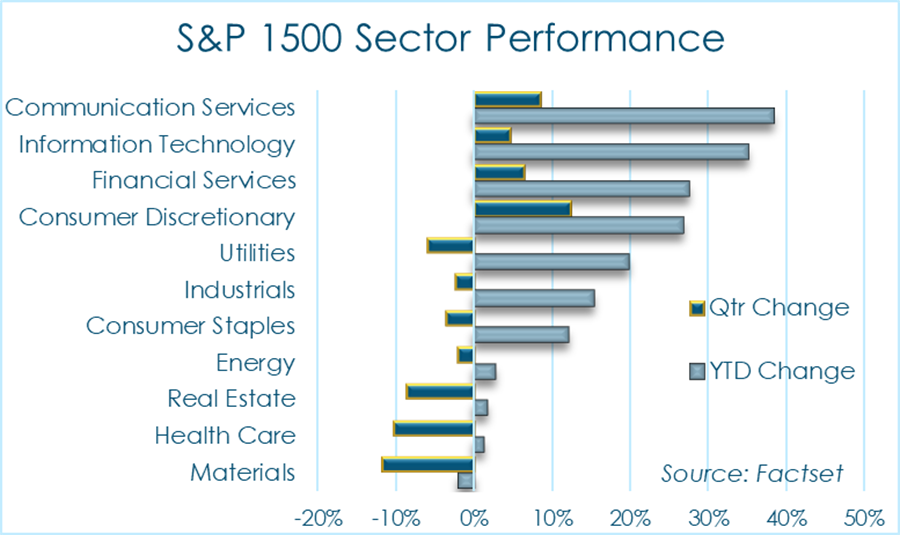

The Magnificent 7 (Apple, Alphabet (Google), Microsoft, Amazon, Meta (Facebook / Instagram), Tesla and Nvidia) continue to drive a significant amount of the overall market’s gain, but their influence waned as the year drew to a close. Investors diversified their portfolios by adding to a broader basket of AI, internet, data center, and software companies in the Communications Services and Information Technology sectors. As the ecosystem of companies investing in and benefitting from AI expands, it’s logical to expect investors to diversify their holdings into those companies which benefit as the ecosystem expands, especially in light of the monumental advances the Mag 7 have had over the last two years and some of their current valuations.

But elevated valuations for some of the Mag 7 hasn’t translated into elevated valuations for all stocks. In fact, equities broadly assessed are not significantly more expensive than they have been on average over the last 10 years when using an inflation-adjusted Free Cash Flow Yield metric. Some investors will cite an elevated Price / Earnings ratio, which is as high as it has been in the last 20 years, but reported earnings are increasingly unrelated to a company’s actual operating results, which is why we prefer inflation-adjusted Free Cash Flow yield to the P/E ratio when looking at valuations.

But elevated valuations for some of the Mag 7 hasn’t translated into elevated valuations for all stocks. In fact, equities broadly assessed are not significantly more expensive than they have been on average over the last 10 years when using an inflation-adjusted Free Cash Flow Yield metric. Some investors will cite an elevated Price / Earnings ratio, which is as high as it has been in the last 20 years, but reported earnings are increasingly unrelated to a company’s actual operating results, which is why we prefer inflation-adjusted Free Cash Flow yield to the P/E ratio when looking at valuations.

From our vantage point, back-to-back years of mid 20% equity market performance is a reasonable investor response to dramatically improving cash flow yields from stocks, initiated by the mega-cap technology companies investing in AI, and trickling down to the broader ecosystem and broader equity market. As such, we do not find stocks unattractively expensive.

Fixed Income

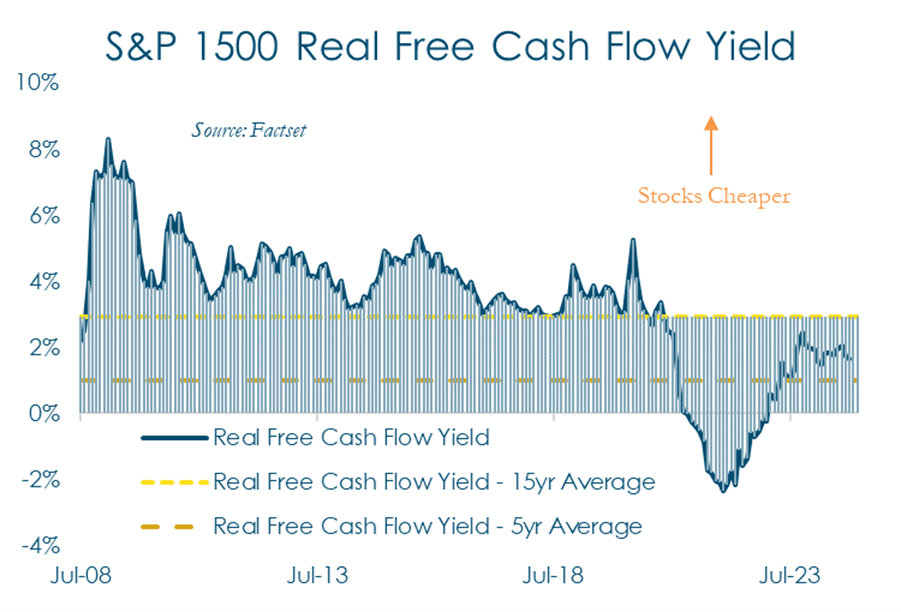

For most fixed income investors, the fourth quarter was not a positive experience. Though yields on short-dated U.S. Treasuries fell, yields on U.S. Treasuries with maturities longer than a year rose, and in some cases, like with the 10-year U.S. Treasury, rose quite dramatically. In fact, bond investors, other than high yield investors, would have lost about 4% during the quarter due to higher rates, depending on the sector, maturity and credit quality.

For most fixed income investors, the fourth quarter was not a positive experience. Though yields on short-dated U.S. Treasuries fell, yields on U.S. Treasuries with maturities longer than a year rose, and in some cases, like with the 10-year U.S. Treasury, rose quite dramatically. In fact, bond investors, other than high yield investors, would have lost about 4% during the quarter due to higher rates, depending on the sector, maturity and credit quality.

The yield spread between investment grade corporate bonds and U.S. Treasuries is as low as it has been in the last 20 years, an indication that bond investors see very little credit risk among corporate bonds, a logical outlook given general economic strength and corporate cash flow results. The largest uncertainty for bond investors at this point is inflation, though we believe bonds offer reasonable protection against inflation given current yields.

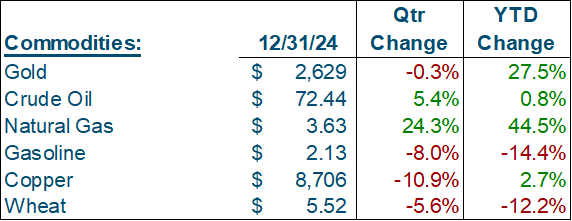

Commodities

Within the commodity complex, natural gas was the standout performer for the fourth quarter and the year, though gold turned in an admirable full-year performance as well.

Within the commodity complex, natural gas was the standout performer for the fourth quarter and the year, though gold turned in an admirable full-year performance as well.

Conclusion

We couldn’t help but cite this statement from Donald Trump because it sums up our hopes for his next stint as president. We hope he learns from the past; widespread tariffs can be disastrous for the American consumer. We hope he approaches trade negotiations pragmatically, defending U.S. intellectual property rights (which are constantly being trampled by China) and negotiates better foreign market access for American producers.

The latter is particularly helpful for small and medium-sized businesses, and why small business optimism spiked after the election. Citing a favorable political climate as the top reason to expand and invest (a factor entirely uncited for most of Biden’s presidency), small business owners expect to increase capital outlays and expand employment because of the election. A net 36% of small businesses expect the economy to improve following the election, versus a net negative 5% prior to the election.

Whether Trump realizes it or not, small businesses are the lifeblood of the U.S. economy, and his trade policies stand to benefit them the most. Small businesses employ, by far, the most people in aggregate and are responsible for the majority of wealth creation in the country. For the past year, small businesses have significantly scaled back their hiring plans, leaving the bulk of payroll gains up to the companies with 500 or more employees. We think that will change, and given the tightness of the labor market, should give employees some incremental negotiating power when it comes to wages and salaries, which should help offset the deleterious effects of elevated inflation on lower income households and support consumer spending.

Under such a scenario, the U.S. would continue to be the world’s standout nation economically and financially. But other economies may also improve; during 2024, an unusually large number of countries held elections in which their citizens delivered similar results; left-leaning progressive candidates and parties largely lost, while right-leaning, more business-centric candidates and parties won. We expect to see a renewed effort among politicians around the world to adopt business-friendly policies as a means to address economic stagnation and consumer frustration with elevated inflation.

We admit that foreign countries may adopt similar negotiating strategies, employing tariffs and other trade barriers against U.S. exports, but currently, the global playing field is not level; U.S. companies face asymmetrical barriers, and given the fact that the U.S. economy is the largest, most diverse and most dynamic, with the wealthiest consumer, and therefore highly attractive to foreign businesses, we suspect that ultimately, foreign politicians will negotiation in good faith, and that global trade will become more fair for U.S. businesses, which is positive for the U.S. economy.

With equity valuations still reasonable and business fundamentals likely to at least remain solid, if not improve further, we expect 2025 to be another solid year economically and financially, something investors will appreciate.