We are strongly committed to returning inflation to our 2 percent goal in support of a strong economy that benefits everyone.

– Federal Reserve Chairman Powell

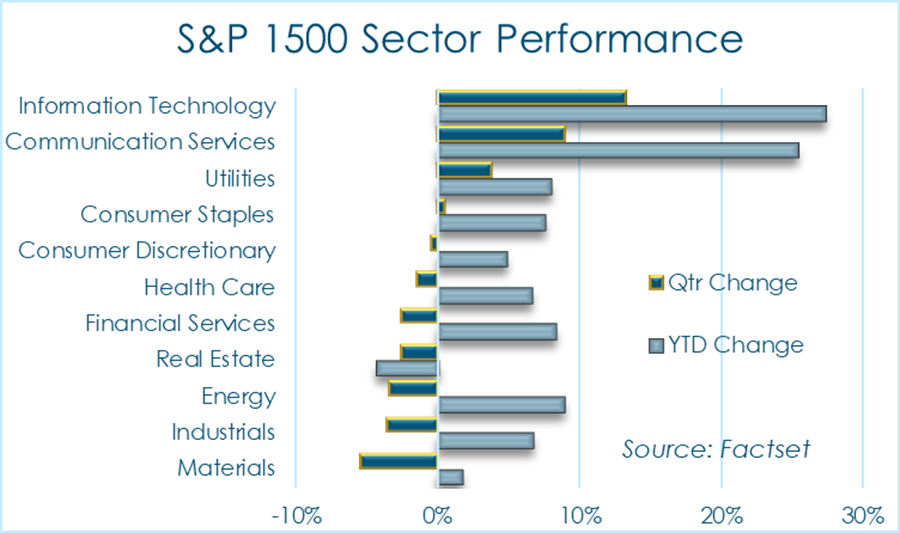

U.S. Equities delivered another positive performance during the second quarter, led once again by information technology and communications stocks, and in particular, a small cadre of the largest companies within those 2 sectors. Investors continue to prefer the large technologically innovative leaders with the massive scale necessary to develop tomorrow’s A.I. platforms.

U.S. Equities delivered another positive performance during the second quarter, led once again by information technology and communications stocks, and in particular, a small cadre of the largest companies within those 2 sectors. Investors continue to prefer the large technologically innovative leaders with the massive scale necessary to develop tomorrow’s A.I. platforms.

Economically, the U.S. maintained much of its strength during the second quarter, once again supported by a favorable labor market and a resilient consumer. However, under the surface, stubbornly high inflation and higher borrowing costs are increasingly stressing households at the lower end of the income and wealth spectrum. Hence, the Federal Reserve’s acknowledgement that, while the economy is strong overall, not everyone is benefiting equally. Monetary policy appears to be restrictive enough to prevent inflation from rebounding, but perhaps not restrictive enough to push it down to its 2% target by year end.

The narrowing of economic activity is playing out similarly within U.S. equities, where “The Magnificent Seven” drove an unusually large share of the total equity gains during the quarter. The fact that these companies are posting market-leading earnings results and generating prolific amounts of free cash flow doesn’t hurt their attractiveness. That said, a higher concentration among advancing stocks typically unnerves investors who see narrowing market leadership as an indication that upward momentum is fading. With gains in six of the last seven quarters, and an upcoming presidential election in which the presumptive candidates are widely disliked, we see a pause or correction and reset as highly likely at some point during the second half of the year.

The Global Economy

Global economic activity during the quarter largely resembled global economic activity during recent quarters; modest overall economic growth characterized by modest strength in services, modest weakness in manufacturing, strong labor markets and moderately elevated inflation overall. Services inflation continues to be the key inflationary factor, even as goods inflation, given the manufacturing sector’s stagnation, has fallen below most central banks’ overall inflation targets.

Global economic activity during the quarter largely resembled global economic activity during recent quarters; modest overall economic growth characterized by modest strength in services, modest weakness in manufacturing, strong labor markets and moderately elevated inflation overall. Services inflation continues to be the key inflationary factor, even as goods inflation, given the manufacturing sector’s stagnation, has fallen below most central banks’ overall inflation targets.

Central banks are keen to begin removing monetary policy restrictions and lower their benchmark interest rates, with an eye towards supporting economic growth. However, during the quarter, inflation’s progress stalled above central bank targets, and because further progress was not evident during the second quarter, central banks have pushed their rate cut forecasts further out, noting, like the Federal Reserve, that further progress with inflation is necessary before they are comfortable removing their policy restrictions.

We’ve written previously about the beneficial influence the normalization of global supply chains and the fading of fiscal stimulus have had on inflation readings, and alluded to the possibility that progress thus far should perhaps be primarily attributed to these factors and less so to higher central bank policy rates. During the quarter, inflation’s stabilization above central bank targets suggests that central bank policies have not had as much impact as previously thought, and that, while absolute central bank benchmark rates are high by recent historical standards, they are not as restrictive as previously assumed.

When setting policy rates, central banks face a major challenge; because economic activity, nationally and internationally, is complex and dynamic, central banks cannot know with certainty what the appropriate benchmark rate should be ex ante. They can only guess, set their rate, and then assess how economic activity transpires over time. Because monetary policy’s effect on economic activity occurs slowly over time, believed to be somewhere between nine and 18 months, central banks must act and then patiently wait before they can glean any insight into whether their policy rates are appropriate.

Considering that rates only became restrictive at the beginning of last year in most major economies, it makes sense that, roughly 18 months later, we are starting to understand that monetary policy may not have had the impact everyone previously believed. Or, perhaps the full effect of previous monetary policy actions have yet to be fully reflected in economic activity, and more specifically, with inflation. We just don’t know.

For the Federal Reserve, this presents an especially challenging dilemma. It can’t know for certain how much effect its prior policy actions will still have on inflation, if any, but it knows that inflation is still too high. The strong labor market notwithstanding, inflation’s deleterious effects on households at the lower end of the income and wealth spectrum is increasingly obvious. Lower income households are less able to handle higher prices for non-discretionary items like food, housing, utilities and insurance. Moreover, higher interest rates, which are based on the Federal Reserve’s benchmark rate, make borrowing more expensive for households at the lower end of the income spectrum because they tend to rely on debt to help fund their standard of living.

For the decade prior to, and then during and immediately after the pandemic, financial disparities between the lower and upper ends of the income and wealth spectrum narrowed, thanks in large part to a decade of low unemployment, low inflation and low interest rates, and then during the pandemic, due to government payments and exceptional unemployment benefits. However, those disparities are now widening; upper income households have larger savings balances that benefit from higher interest rates on savings, larger investment portfolios that benefit from strong equity market performance, and they borrow less. Consumer measures for the upper income households remain quite strong. On the other hand, delinquency and charge-off rates for consumer loans and credit cards are steadily rising among lower income households.

From a purely pragmatic perspective, financial stress among lower income households does not pose a significant threat for the overall economy since the majority of discretionary consumer spending happens within upper income households. But this perspective ignores the humanitarian foundation of the economy and as such, the Federal Reserve is acutely aware of and highly sensitive to this bifurcation. It hopes that by delaying interest rate reductions, which would benefit low income households, it can tame inflation faster, and then lower its benchmark rate, providing dual relief to lower income households.

In this regard, the economic data during the quarter suggest further progress with inflation is likely. The labor market continues to come into a better balance, and activity within the services sector, which has been the source of most inflationary pressures, appears to be slowing. As such, if inflation improves during the second half of the year, the Federal Reserve may reduce its benchmark rate once or twice towards the end of the year. But we first need to see inflation resume its downward trend, something that we suspect will happen during the third quarter, based on companies’ comments during recent earnings calls.

Equities

Against this backdrop, equities rose during the quarter, but not all companies participated equally. For example, the headline S&P 500 Index is a market capitalization weighted index that derives a stock’s contribution based on its size, making large companies more important to the index’s performance and small companies less so. This index rose nearly 4% for the quarter. But S&P also tracks an equal-weighted index of the same companies that assigns each stock the same weight; the equal weighted index fell 3% during the quarter, an indication that equity market strength is not as broad-based as it may appear on the surface.

Against this backdrop, equities rose during the quarter, but not all companies participated equally. For example, the headline S&P 500 Index is a market capitalization weighted index that derives a stock’s contribution based on its size, making large companies more important to the index’s performance and small companies less so. This index rose nearly 4% for the quarter. But S&P also tracks an equal-weighted index of the same companies that assigns each stock the same weight; the equal weighted index fell 3% during the quarter, an indication that equity market strength is not as broad-based as it may appear on the surface.

It may be a year since Microsoft’s A.I. announcement but A.I. still dominates the market narrative. The Magnificent Seven garner the bulk of the media attention, but tech titans around the world are investing staggering amounts in their A.I. offerings and tools, which supports an entire ecosystem of chip makers like Nvidia, their manufacturing partners, and semiconductor capital equipment and tools suppliers and services. A.I.’s massive power demands have become the most important paradigm shift for the utilities sector in more than 50 years.

But the performance discrepancy extends beyond the A.I. narrative. These same seven companies are driving current earnings results for the entire market. To wit, during the first quarter, earnings among all S&P 500 companies rose nearly 6% year over year, while earnings for all companies other than the Magnificent Seven fell nearly 2%. During April and May, we noted a step-up in the number of companies citing more cautious customer behavior and value-conscious consumers trading down in an effort to relieve some inflationary pressures.

Although the macro-economic data suggest inflation has stalled, the micro-commentary among companies suggests that further inflationary progress is probable. While that’s welcome news for the Federal Reserve and lower income households, it may not be welcome news for companies or investors. Weaker pricing power, unless it’s accompanied by lower input costs, compresses profit margins and cash flow, something that is currently not envisioned by investors for the remainder of this year or next. In fact, investors expect earnings growth to accelerate during the second half of the year and reach 10% next year. The Magnificent Seven are certainly an important element within that, but other sectors such as consumer discretionary, financials, materials, utilities and health care are expected to contribute meaningfully to the reacceleration of earnings growth. Combined with somewhat elevated valuations, the second half of 2024 may not be as easy or straightforward as the first.

Fixed Income

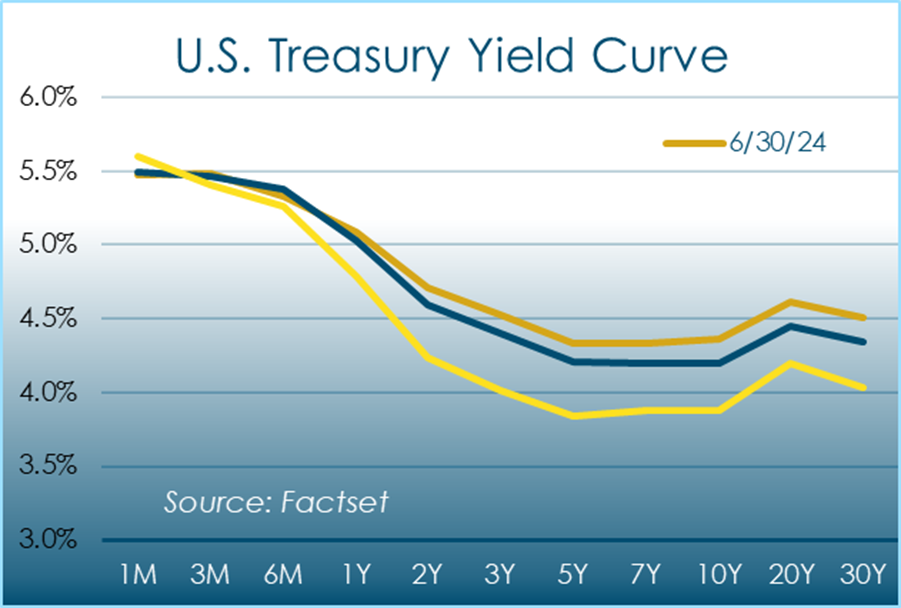

As it became clear that the Federal Reserve would not lower its benchmark rate this summer, yields on U.S. Treasuries rose. Investors are still concerned that higher fiscal deficits and lower Federal Reserve buying will drive yields even higher, but investors appeared to be taking those in stride during the quarter. Corporate bonds were relatively unchanged during the quarter and remain in negative territory performance-wise for the year.

As it became clear that the Federal Reserve would not lower its benchmark rate this summer, yields on U.S. Treasuries rose. Investors are still concerned that higher fiscal deficits and lower Federal Reserve buying will drive yields even higher, but investors appeared to be taking those in stride during the quarter. Corporate bonds were relatively unchanged during the quarter and remain in negative territory performance-wise for the year.

Commodities

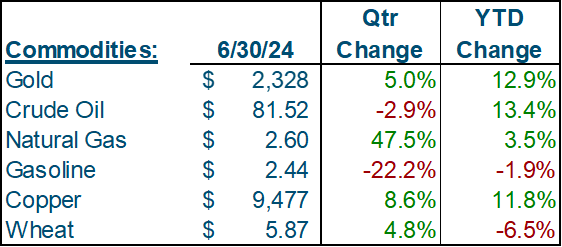

In the commodity complex, copper built on its first quarter gain as investors increasingly grapple with what is likely to be a medium-term copper supply shortage. It’s much easier to envision an all-electric economy, but installing the infrastructure to support it won’t be as easy.

In the commodity complex, copper built on its first quarter gain as investors increasingly grapple with what is likely to be a medium-term copper supply shortage. It’s much easier to envision an all-electric economy, but installing the infrastructure to support it won’t be as easy.

Conclusion

In our last quarter’s Review, we shared our belief that the Federal Reserve has placed the U.S. economy on a glide path to a Goldilocks scenario (strong and balanced labor market, modest inflation, and normalized interest rates) that generates moderate economic growth over multiple years. Inflation’s stall during the second quarter doesn’t threaten that potential outcome as much as it simply delays the onset of it. Lower income households could use some relief now, but if the Federal Reserve unwinds its policy stance too early, inflation could rebound, and the subsequent environment would be even worse for them. So, while it’s painful for the time being, we expect that during the second half of the year, inflation will resume its downward march, companies will expand their efforts to reduce the inflationary burden on their customers, and that in 2025, we will enter a multi-year period where the economy works for everyone.