Freedom is not a gift bestowed upon us by other men, but a right that belongs to us by the laws of God and nature. – Benjamin Franklin

As America prepared to celebrate its 250th birthday this past weekend, the fireworks arrived early for investors. Familiar themes driven by technological innovation powered stocks to all-time highs, more than offsetting a moderately weak first quarter.

As America prepared to celebrate its 250th birthday this past weekend, the fireworks arrived early for investors. Familiar themes driven by technological innovation powered stocks to all-time highs, more than offsetting a moderately weak first quarter.

Artificial Intelligence continues to dominate the narrative for investors. Without question, it’s also a tailwind for the U.S. economy. But to ascribe the U.S.’ solid economic growth entirely to the A.I. investment boom would misrepresent what is in reality, broad strength across virtually every sector of the economy. Although the labor market froze somewhat after “Liberation Day” last April, recent data suggest labor demand is picking up while the duration of unemployment is declining. Wage growth continues to outpace inflation, which in turn allows households to spend, reduce their debt and build their savings simultaneously.

With that said, we are closely watching whether companies are reducing their headcounts as they adopt A.I. or whether investor enthusiasm has become untethered from reasonable expectations, signaling that another investment bubble is building. We see neither at the moment.

Rather, we see the country’s foundational characteristics, liberty, private property, and free enterprise, as poised to usher in a new chapter of U.S.-led innovation, one in which A.I. and quantum computing are deployed simultaneously to unlock breakthroughs in advanced materials science, healthcare, and communications. And we see American companies at the forefront of those innovations.

Which is why we can’t help but feel immense pride to be American, optimistic for our future. Our inalienable rights to life, liberty and the pursuit of happiness, safeguarded by our constitution, have carried us for the first 250 years and, God willing, will carry us for another 250 years. May God Bless America this July 4th.

The Global Economy

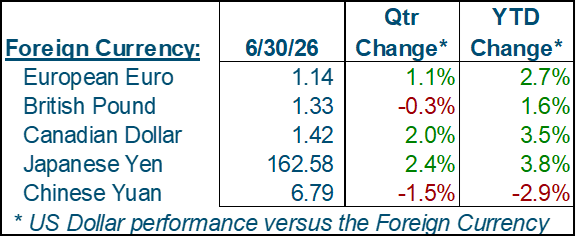

Pressure on the global economy mounted during the second quarter as Iran’s closure of the Strait of Hormuz became more evident as the quarter progressed. The effective cessation of oil transport to Asia and Europe pushed inflation higher and slowed economic activity, as both businesses and consumers grew more cautious. The situation is more acute in Europe, where economic growth was already near zero before the European Central Bank had to raise its benchmark rate as a precautionary measure to prevent accelerating inflation from accelerating even faster.

Pressure on the global economy mounted during the second quarter as Iran’s closure of the Strait of Hormuz became more evident as the quarter progressed. The effective cessation of oil transport to Asia and Europe pushed inflation higher and slowed economic activity, as both businesses and consumers grew more cautious. The situation is more acute in Europe, where economic growth was already near zero before the European Central Bank had to raise its benchmark rate as a precautionary measure to prevent accelerating inflation from accelerating even faster.

In the U.S., broad economic activity continues to exceed expectations. Recall that despite an unemployment rate in the low to mid 4% range, towards the end of last year and the early part of this year, recent college graduates and lower-skilled workers struggled to find gainful employment. This “no hire / no fire” situation appears to be improving. Job openings rose during the quarter and the number of unemployed declined, suggesting companies are regaining confidence and expanding their payrolls.

Despite widespread fears that A.I. adoption would result in layoffs, the data thus far suggest companies are adopting A.I. as an augmentation, not a replacement, for their labor force. That would bode well for recent college graduates which tend to be among the most technologically savvy and would potentially be among the most productive users of A.I. tools in the workplace.

The labor market strength explains why consumer spending held up well during the quarter, despite significantly higher gasoline prices. Under the surface, more discretionary categories like food away from home and entertainment and leisure continue to benefit from consumers wanting to enjoy experiences. Household financial conditions continue to strengthen, and though inflation-adjusted after-tax disposable income stalled during the quarter because inflation rose on higher gasoline prices, with oil and gasoline prices falling, we expect this foundational element of consumer spending to reaccelerate this year.

In the meantime, credit card delinquencies continue to decline, more consumers are making full balance payments every month, mortgage and consumer credit as a percentage of disposable personal income is at a 30-year low, and household wealth is at an all-time high. Consumer confidence remains pessimistic, but consumers notoriously complain when answering surveys while spending with confidence. For investors, the labor market, consumer spending and general economic activity are all positive signals.

Equities

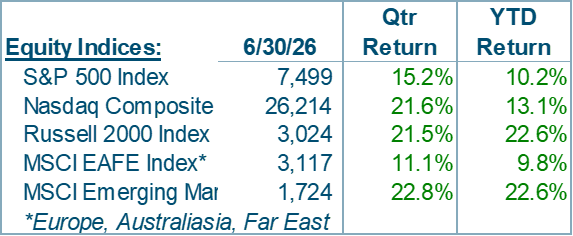

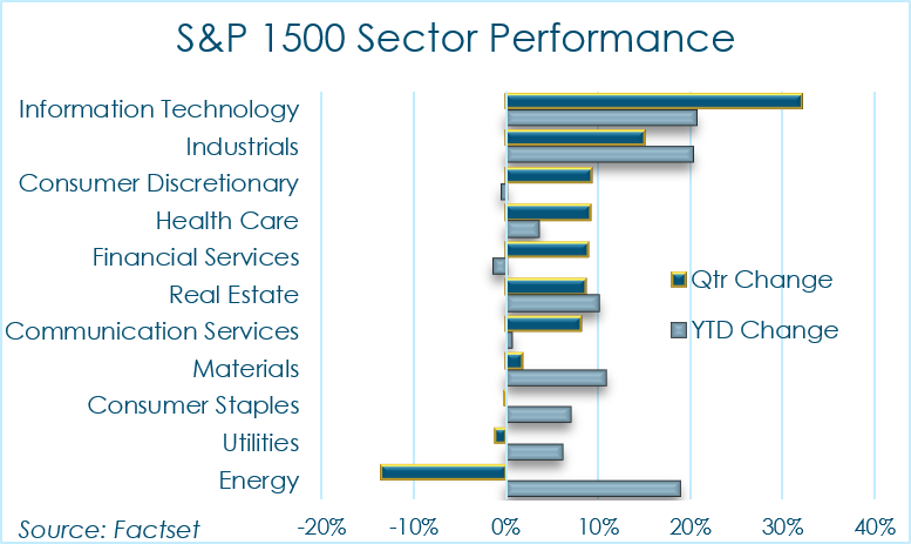

Equities performed exceptionally well during the second quarter, turning in the best quarterly performance since the second quarter of 2020, which benefitted from the Federal Reserve’s bond-buying efforts to backstop financial markets in the midst of Covid panic selling. Technology was, once again, the standout sector.

Equities performed exceptionally well during the second quarter, turning in the best quarterly performance since the second quarter of 2020, which benefitted from the Federal Reserve’s bond-buying efforts to backstop financial markets in the midst of Covid panic selling. Technology was, once again, the standout sector.

Semiconductor stocks surged 88% during the quarter; Data Center demand for memory chips (to support A.I. computing demand) exceeds memory chip supply, and because it takes at least two years to add new greenfield manufacturing capacity, demand is likely to exceed supply well into 2027 if not 2028. There are now 16 stocks globally valued at more than $1 trillion, the largest being Nvidia at $5 trillion. Twelve of these 16 stocks are in the technology sector (13 if you include SpaceX as a technology stock), and 13 of the 16 are U.S. companies (none are Chinese). Elon Musk runs two of the 16 (Tesla and SpaceX).

Outside of technology, strength was broad-based with multiple sectors delivering high single-digit % gains. We attribute the broad-based strength to very strong earnings results in the first quarter; first quarter earnings grew on average 29% compared to investor expectations for 13%. Perhaps more importantly, investors raised their expected earnings growth for the rest of 2026 to 23%, up from 16% at the end of March, and to 14% for 2027, up from 7% at the end of March.

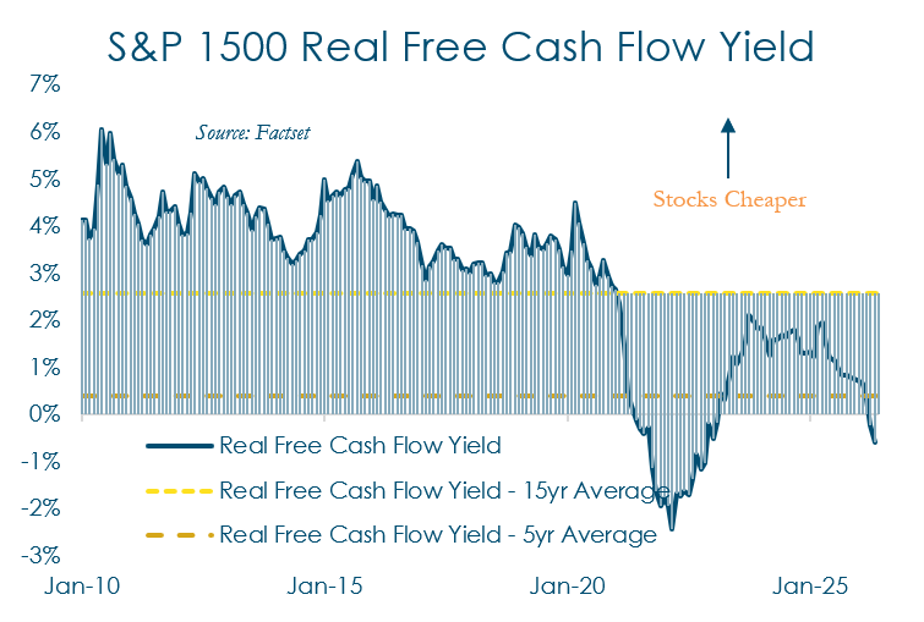

Valuations also played a role in the second quarter’s strength; For most sectors, Price / Earnings ratios rose modestly during the quarter, which, when combined with strong earnings, produces very strong equity market performance. From a historical context, stocks are expensive, trading above their 5-year and 15-year average valuations. Part of the elevated valuations historically is attributable to inflation, which reduces the market’s overall inflation-adjusted Free Cash Flow Yield, our preferred metric to assess valuations. Prior periods in which stocks were expensive using this metric also coincided with high inflation; we expect that with oil prices falling, inflation will attenuate, inflation-adjusted free cash flow yield will rise, and stock prices won’t appear to be as expensive as they appear to be now.

Valuations also played a role in the second quarter’s strength; For most sectors, Price / Earnings ratios rose modestly during the quarter, which, when combined with strong earnings, produces very strong equity market performance. From a historical context, stocks are expensive, trading above their 5-year and 15-year average valuations. Part of the elevated valuations historically is attributable to inflation, which reduces the market’s overall inflation-adjusted Free Cash Flow Yield, our preferred metric to assess valuations. Prior periods in which stocks were expensive using this metric also coincided with high inflation; we expect that with oil prices falling, inflation will attenuate, inflation-adjusted free cash flow yield will rise, and stock prices won’t appear to be as expensive as they appear to be now.

Fixed Income

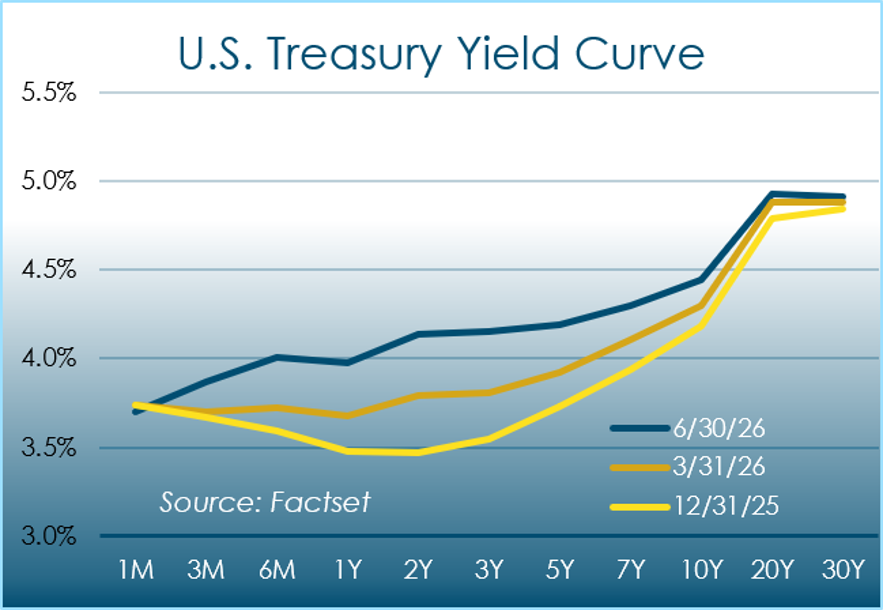

Accelerating inflation pushed yields on U.S. Treasuries higher during the quarter, but Kevin Warsh’s first meeting as Federal Reserve chair also surprised investors with how focused he was on taming inflation. Investors had to abandon expectations that the Fed would lower rates this year. We think with lower oil prices the rest of the year, inflation will moderate and while the Fed may not lower rates, at the very least, rate increases appear to be off the table.

Accelerating inflation pushed yields on U.S. Treasuries higher during the quarter, but Kevin Warsh’s first meeting as Federal Reserve chair also surprised investors with how focused he was on taming inflation. Investors had to abandon expectations that the Fed would lower rates this year. We think with lower oil prices the rest of the year, inflation will moderate and while the Fed may not lower rates, at the very least, rate increases appear to be off the table.

Commodities

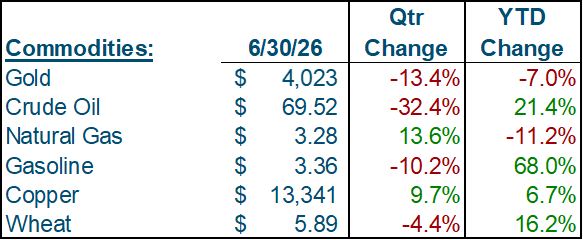

Oil prices declined during the quarter after the U.S. and Iran agreed to a cease fire that included an agreement by both parties to allow shipping to pass through the Strait of Hormuz. We expect that over time, shipping will approach previous levels and that with oil supply to Asia and Europe recovering, oil prices in the U.S. will also remain relatively steady. With U.S. Treasury prices higher and the prospects for lower inflation, Gold also struggled.

Oil prices declined during the quarter after the U.S. and Iran agreed to a cease fire that included an agreement by both parties to allow shipping to pass through the Strait of Hormuz. We expect that over time, shipping will approach previous levels and that with oil supply to Asia and Europe recovering, oil prices in the U.S. will also remain relatively steady. With U.S. Treasury prices higher and the prospects for lower inflation, Gold also struggled.

Conclusion

The United States comprises 4% of the world’s population but generate 25% of its economic output. The total value of all U.S. publicly traded companies represents approximately half of the total value of all publicly traded companies globally; the U.S. market alone is worth more than the next 9 countries’ markets combined. Without question, the U.S. is the world’s most innovative, most efficient, and most productive society.

We can thank the system of liberties we enjoy for our success. These liberties create opportunity, which, alongside private property rights and an entrepreneurial spirit, inspire innovation and creativity, which ultimately lead to prosperity. This July 4th is an opportunity to reflect with gratitude on the wisdom our founding fathers possessed and their efforts to enshrine that wisdom in a Constitution that facilitates the benefits we all enjoy today. God Bless America.