The Fog of War – McDonald Clarke

The first quarter of 2026 has proven challenging for investors, on both the equity and fixed income sides. Joint U.S. and Israeli strikes on Iran and Iran’s response to block traffic passing through the Strait of Hormuz dented investor confidence, which had pushed U.S. equity indices to all-time highs in January. As the quarter drew to a close, uncertainty regarding the Administration’s goals, potential duration of the conflict, and medium-term consequences on economic activity left both U.S. equities and bond prices in the red.

The first quarter of 2026 has proven challenging for investors, on both the equity and fixed income sides. Joint U.S. and Israeli strikes on Iran and Iran’s response to block traffic passing through the Strait of Hormuz dented investor confidence, which had pushed U.S. equity indices to all-time highs in January. As the quarter drew to a close, uncertainty regarding the Administration’s goals, potential duration of the conflict, and medium-term consequences on economic activity left both U.S. equities and bond prices in the red.

Near-term visibility is poor; the conflagration of interests and intentions, some of which are purposefully opaque, among the U.S., Israel, Iran, and the half-dozen Gulf nations embroiled in the conflict pose a daunting array of variables to consider, all of which depend upon the decisions of a notoriously unpredictable president. Uncertainty is not one-sided though; on the final trading day of the quarter, stocks rebounded sharply after rumors that Iran wanted to begin formal negotiations pushed oil prices down and forced investors to cover some of their short positions. In this sense, being out of the market could be just as risky as remaining fully invested, which is why we think it’s futile to attempt to trade with a short-term perspective.

In the medium term, we see certain possibilities as more likely than others. Because we believe an extended U.S. military occupation of Iran is a low probability, the Islamic theocracy in Iran is more likely to survive than not, which suggests that some degree of ongoing conflict in the middle east likely creates structurally higher energy prices and somewhat lower discretionary consumer spending. Military spending is likely to be higher, creating modestly higher fiscal deficits, which in turn will likely set a higher floor for interest rates. We see little impact on equities overall, though individual sectors may face headwinds while others enjoy tailwinds. Admittedly, our confidence in this medium-term outlook is moderate; we are, after all, still in the fog of war.

The Global Economy

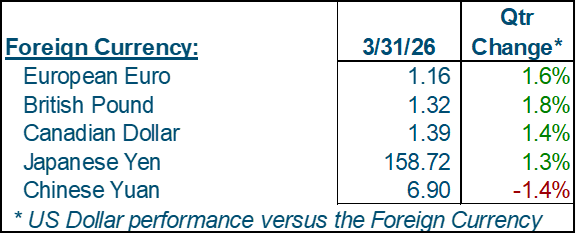

At the start of 2026, the global economy’s ongoing recovery from last year’s “Independence Day” tariff shock was increasingly evident. But joint U.S. and Israeli strikes against Iran and Iran’s subsequent decision to block shipping through the Strait of Hormuz, through which 20m barrels of oil pass daily (roughly 20% of global oil supply / demand), threatens to alter the short-term trajectory of global economic activity, especially for Asia and Europe which rely heavily on oil, distillates and natural gas (which is also a key input for the production of fertilizer) from the middle east.

At the start of 2026, the global economy’s ongoing recovery from last year’s “Independence Day” tariff shock was increasingly evident. But joint U.S. and Israeli strikes against Iran and Iran’s subsequent decision to block shipping through the Strait of Hormuz, through which 20m barrels of oil pass daily (roughly 20% of global oil supply / demand), threatens to alter the short-term trajectory of global economic activity, especially for Asia and Europe which rely heavily on oil, distillates and natural gas (which is also a key input for the production of fertilizer) from the middle east.

China, Japan and South Korea are all vulnerable to oil and natural gas supply disruptions. China sources about half of its oil from the Middle East, excluding Iran, whereas Japan sources nearly 95% of its oil from the Middle East. Although China has made more progress transitioning to electric vehicles than Japan and South Korea, (10% of the on-the-road fleet versus 3% in Japan and South Korea), all three countries rely on gasoline for the vast majority of consumer transportation. China has 100 days’ worth of oil in its strategic reserves whereas Japan and South Korea have more than 200 days’ in strategic reserves. Although the impact to consumers will materialize sooner in China than Japan and South Korea, all three will face consumer spending headwinds and accelerated inflation if the Strait remains closed or restricted for an extended period of time.

In Europe, the challenge is two-fold; natural gas is a key source for household heat (75% in the U.K. and nearly 40% in the Eurozone), and with 95% of the cars on the road using internal combustion engines and only 90 days’ worth of oil in strategic reserves, both the U.K. and the Eurozone consumer will feel the pinch of higher gasoline prices immediately. After diversifying its natural gas supply from Ukraine in 2022 to rely more heavily on Qatar, Europe is once again confronted with an LNG import challenge and likely responds by pushing renewable energy even harder, but it will take time. Thankfully, Europe has time to build its natural gas inventories before winter sets in and heating-related demand returns.

The U.S. is perhaps the best positioned among major economies to weather the impact of higher oil and gas prices coming out of the middle east, in part because unlike Asia and Europe, the U.S. is energy independent. Without question, higher global oil prices will mean higher domestic oil prices, but if the medium-term outlook for oil prices remains elevated (not our base case), domestic producers will respond with higher production which will in turn prevent oil prices from spiking to the same extent they could internationally. Domestic producers require around $60 / barrel to profitably drill new wells; at $100 / barrel, the profit motive is highly enticing.

In the meantime, the U.S. economy remains on solid footing. Despite a surprisingly sharp decline in non-farm payroll additions in February, on the whole, labor market conditions are solid and steady; non-farm payroll additions during January were strong, the unemployment rate continues to hover in the low- to mid-4% range, and jobless claims show no indication that businesses are shedding employees. With the government’s working-age population estimate revisions in January, there now appears to be less slack in the labor market than previously estimated, a welcome development for recent college graduates who have struggled to find employment directly out of school. In fact, we expect recent college graduates to fare much better this year as companies begin to deploy AI and will need tech-savvy graduates to help implement and use it (AI appears to be a net-positive for job creation right now).

Although $4 gasoline prices are suddenly a shock for all drivers, the threat to consumer spending is modest, in our opinion. The majority of consumer spending over the last two years has come from upper income households who are most capable of absorbing higher gasoline prices without having to adjust their spending. With a strong labor market, employees continue to enjoy wage growth that exceeds inflation, household balance sheets are in good shape, and despite what consumers are saying in surveys, they continue to spend at a sufficient pace to keep the U.S. economy growing at or above its long-term trend.

Which is why investor expectations for the Federal Reserve are not drastically different today than they were before hostilities began. Multiple Federal Reserve officials have publicly stated they are willing, for the time being, to look past higher gasoline prices believing them to be temporary. We also note that the Federal Funds rate is still modestly restrictive, which is inherently anti-inflationary. Accordingly, rate hikes do not appear to be on the table, a positive for equities.

Equities

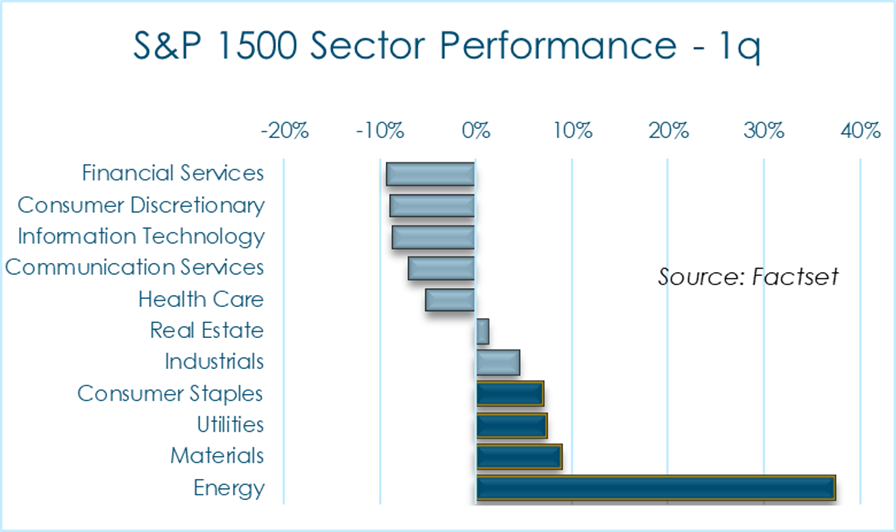

Equity investors adopted a defensive posture in response to the U.S. and Israeli attack on Iran, selling Information Technology and Communication Services and moving into Utilities, Consumer Staples and Energy. Our sources suggest that investor allocations to Information Technology and Communication Services are now at 30-month lows and that investors have sold 3.7b shares short, the highest on record. In a nutshell, investor sentiment is quite negative.

Equity investors adopted a defensive posture in response to the U.S. and Israeli attack on Iran, selling Information Technology and Communication Services and moving into Utilities, Consumer Staples and Energy. Our sources suggest that investor allocations to Information Technology and Communication Services are now at 30-month lows and that investors have sold 3.7b shares short, the highest on record. In a nutshell, investor sentiment is quite negative.

This negativity appears to be short-term tactical, however. Companies reported earnings growth for the fourth quarter of 2025 (reported during the first quarter of 2026) nearly double what investors expected, and while first quarter earnings estimates didn’t climb much, estimates for full-year 2026 earnings growth are now a heady 16.5%. We will watch closely what companies say during their first quarter calls in April and May (the Iran conflict had not started when the majority of companies announced their earnings and provided 20206 guidance), and while we expect companies to use the hostilities as a basis for caution, we don’t expect significant downward revisions to their guidance.

With stock prices down and earnings estimates up, valuation ratios fell during the quarter. Valuations are now much closer to their 10-year historical averages on most metrics, a potentially attractive set up for equities going forward if the middle east conflict is resolved quickly, there are no major lingering disruptions to oil and natural gas supplies, and companies continue to execute on their growth plans as they have recently. This is potentially one of the better buying opportunities we’ve had in some time, especially for technology stocks.

Fixed Income

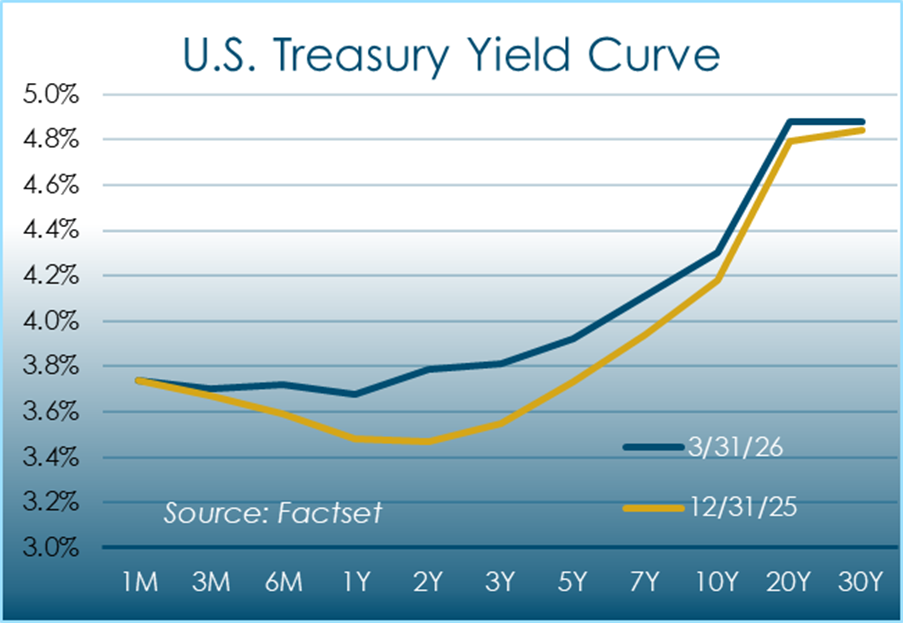

After falling modestly during January and February, U.S. Treasury yields spiked in March, but paradoxically, not because of the risk higher oil prices present for inflation over the medium or long-term. Rather, investors are (correctly) looking through the temporary oil price shock and appear to be pricing in 1) a higher Federal Reserve “neutral” rate than they were previously, and 2) the potential for higher U.S. government spending on military equipment and munitions, which would manifest itself in higher U.S. Treasury issuance over the next few years (higher supply pushes bond prices down and yields up). The fact that the yield curve moved most around the 2-year maturity indicates investors see this as a 2-year phenomenon, not a long-term structural phenomenon.

After falling modestly during January and February, U.S. Treasury yields spiked in March, but paradoxically, not because of the risk higher oil prices present for inflation over the medium or long-term. Rather, investors are (correctly) looking through the temporary oil price shock and appear to be pricing in 1) a higher Federal Reserve “neutral” rate than they were previously, and 2) the potential for higher U.S. government spending on military equipment and munitions, which would manifest itself in higher U.S. Treasury issuance over the next few years (higher supply pushes bond prices down and yields up). The fact that the yield curve moved most around the 2-year maturity indicates investors see this as a 2-year phenomenon, not a long-term structural phenomenon.

Commodities

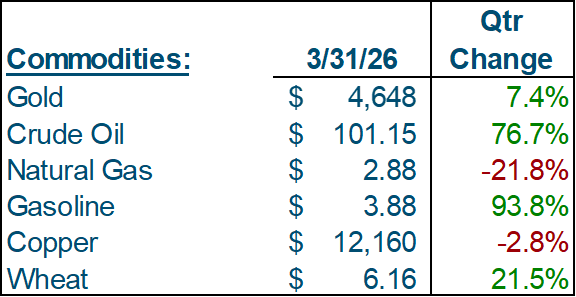

It’s no surprise that oil and gasoline were the standout movers during the first quarter. With that said, we expect oil prices to retreat once hostilities have ceased. With 80 million barrels of oil in storage “on the water” and tens of millions of additional barrels stored in export terminals waiting to be loaded onto tankers for delivery, once the Strait opens to traffic and that supply hits the market, oil prices should fall quickly. They may not fall back to their pre-Iran levels of $60 / barrel because ongoing tensions in the region will support a structurally higher oil price but underlying global supply / demand dynamics remain titled towards a modest global over-supply, which will keep a lid on oil prices through the remainder of 2026.

It’s no surprise that oil and gasoline were the standout movers during the first quarter. With that said, we expect oil prices to retreat once hostilities have ceased. With 80 million barrels of oil in storage “on the water” and tens of millions of additional barrels stored in export terminals waiting to be loaded onto tankers for delivery, once the Strait opens to traffic and that supply hits the market, oil prices should fall quickly. They may not fall back to their pre-Iran levels of $60 / barrel because ongoing tensions in the region will support a structurally higher oil price but underlying global supply / demand dynamics remain titled towards a modest global over-supply, which will keep a lid on oil prices through the remainder of 2026.

Conclusion

It is sometimes hard to separate our personal feelings and desires from our professional obligations and duties; now is one of those times. As much as we wish the U.S. would destroy the Revolutionary Guards, liberate the Iranian people and set the stage for more peaceful relations among the middle east nations, Trump’s America First policy and the lessons from prior regime change efforts in the middle east preclude that likelihood. What we’re left with instead is the probable survival of the Islamic theocracy that, though severely diminished militarily, will be more hardline than before, firmly resolved to oppress its citizens, antagonize its neighbors, threaten the global economy, and ultimately, resume its clandestine attempts to develop nuclear weapons. Without regime change in Iran, the threat to the U.S. and the middle east never goes away, but we doubt the time has come for the U.S. to bring it about.

In the meantime, for U.S. investors, the medium-term outlook overall is relatively unchanged, even if the specific opportunities have changed. Significantly lower valuations for Information Technology stocks create a potential buying opportunity, whereas strength in defensive sectors and Energy likely make them vulnerable to weakness once risk appetites return. Consumer discretionary stocks, especially those catering towards the middle- and higher-income demographics are likely to perform well. And of course, military contractors are likely to see a structural lift in demand for their products and services.

With that said, we must note that our confidence in our outlook is only moderate; visibility, especially in the near-term, is poor; the situation is fluid and can change quickly if Trump decides to occupy Iran or attempts to change the regime. We, like everyone else, are caught in the fog of war.