…we believe that our policy rate is likely at or near its peak for this tightening cycle…

– Federal Reserve Chairman Jerome Powell

2023 ended in appropriate fashion, with impressive returns to cap a year of impressive returns. Investors rang in the New Year optimistic the Federal Reserve has guided the economy into a goldilocks scenario of diminishing inflation without significantly disrupting the labor market or consumer.

2023 ended in appropriate fashion, with impressive returns to cap a year of impressive returns. Investors rang in the New Year optimistic the Federal Reserve has guided the economy into a goldilocks scenario of diminishing inflation without significantly disrupting the labor market or consumer.

Without dismissing a variety of risk factors that could still lead to a mild recession, economic data during the fourth quarter suggest a goldilocks scenario is increasingly plausible. Supply chain disruption, as is now clear, contributed materially to inflation’s surge, as did unprecedented fiscal stimulus during 2020 and 2021. As both factors recede into the rear-view mirror, their influence on inflation recedes, leaving a resilient labor market and a consumer that is relatively healthy, both of which continue to fuel healthier economic activity than most investors and economists had anticipated.

The seemingly best-case scenario economically is not necessarily a best-case scenario for investors, however. 2023’s strong equity market gains demonstrate that investors increasingly expect a goldilocks economy accompanied by lower interest rates, and bid up stock prices as a result. Although we don’t believe stock valuations overall are unattractive, because they are somewhat elevated relative to both their historical average and relative to other asset classes like investment grade bonds, the attractiveness of their risk / reward profile is somewhat diminished.

Which poses a dilemma; even if economic activity meets investor expectations, elevated equity valuations will likely blunt stock market gains in 2024. In other words, stocks may perform positively in 2024, but investors should temper their expectations and exercise discipline when making decisions.

The Global Economy

Global economic activity weakened into and through the fourth quarter but was still positive overall. Encouragingly, global inflation continued to improve, and as such, most central banks have shifted from a tightening / inflation-fighting bias to somewhere between a neutral or loosening / economically supportive bias.

Global economic activity weakened into and through the fourth quarter but was still positive overall. Encouragingly, global inflation continued to improve, and as such, most central banks have shifted from a tightening / inflation-fighting bias to somewhere between a neutral or loosening / economically supportive bias.

In China, declining exports, stagnation in the manufacturing and services sectors, rising property-sector bankruptcies and debt restructuring, and a general flight of capital from the country (both financial and physical) because of geopolitical concerns all weigh on economic growth. In Japan, modestly positive economic activity in the fourth quarter will prevent the country from experiencing a technical recession, but a lackluster performance in 2024 appears inevitable.

Unlike Japan, Europe probably entered a recession in the fourth quarter due to persistent weakness within its manufacturing, industrial, and services sectors, coupled with persistently negative consumer confidence. On the positive side, inflation continues to fall, opening the door for the European Central Bank to begin lowering rates in order to provide some stimulus.

In the U.S., economic activity moved decisively closer to a soft-landing scenario in which inflation returns to 2% without the onset of a recession. The labor market remains strong, job openings still exceed the number of unemployed individuals but by a more reasonable margin, and labor market separations, both voluntary (quits) and involuntary (layoffs) are steady. Concerns we raised in the third quarter about rising jobless claims and expanding unemployment duration appear to have been premature, as both have stabilized at low levels. Perhaps most importantly, labor productivity improved coming into the end of the year, a factor that always plays a critical role with employee compensation, consumer spending, company profit margins, and inflation.

Labor market and consumer spending strength notwithstanding, activity within the manufacturing sector continues to flash recession warning signs. New manufacturing orders have declined since July 2022 and backlogs have declined since October 2022. As a result, for the last 18 months, manufacturers have relied on their backlogs to maintain production levels, but, after rising to historic levels exiting the pandemic, manufacturing backlogs have returned to, or in some cases, below historical averages, and now, total production is stagnating. Moreover, as the year drew to a close, the services sector also slowed noticeably, which has important implications for inflation, the Federal Reserve’s primary focus at the moment.

In this regard, the Federal Reserve is pleased to see inflation falling steadily. Although it’s too early to take a victory lap, inflation in the 2% – 3% range, depending on the measure and whether food and energy are included or excluded, is approaching the Fed’s stated goal of 2% over the long term. Which is why Jerome Powell and other governors are comfortable publicly declaring that its efforts to bring inflation down are close to completion, and that, at some point in 2024, it will be appropriate to unwind some of the policy restrictions it enacted in 2022 and 2023. Hence, investor enthusiasm that the end of the rate-raising phase has arrived and that more supportive monetary policy is around the corner.

Equities

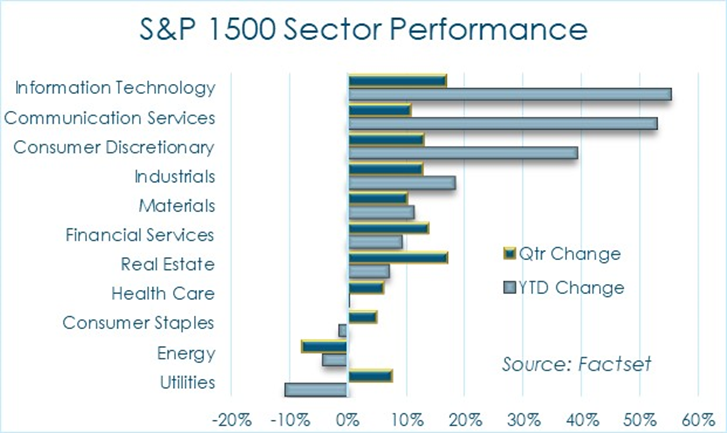

Given the economic backdrop and the shift in Federal Reserve policy, it shouldn’t come as a surprise that equities performed well in 2023. It may, however, be surprising just how well certain individual equities performed, like NVIDIA (NVDA, up 239%), Meta, owner of Facebook and Instagram (META, up 194%), or Uber (UBER, up 149%).

Given the economic backdrop and the shift in Federal Reserve policy, it shouldn’t come as a surprise that equities performed well in 2023. It may, however, be surprising just how well certain individual equities performed, like NVIDIA (NVDA, up 239%), Meta, owner of Facebook and Instagram (META, up 194%), or Uber (UBER, up 149%).

Because of the nature of how equity indices are constructed and how their returns are calculated, the largest companies have the largest weights within the index, and therefore, have the potential to influence the index returns the most. We noted during the year, as did many others, that although the broad equity market returns were impressive, a relatively small number of stocks drove the majority of those gains. To wit, the S&P 500 equal-weighted index, where every stock has the same weight and the same contribution to the index return, only gained 11.7%, a far cry from the market-cap weighted S&P 500 index, which gained 24%.

Interestingly, rising economic optimism has yet to be reflected in 2024 earnings estimates, which declined slightly during the fourth quarter. If stock prices rise when earnings fall or are flat, Price / Earnings multiples rise, which is exactly what occurred during the fourth quarter. Using the conventional Price / Earnings multiple, stocks are more expensive at the end of the year and now trade 22% above their historical Price / Earnings average.

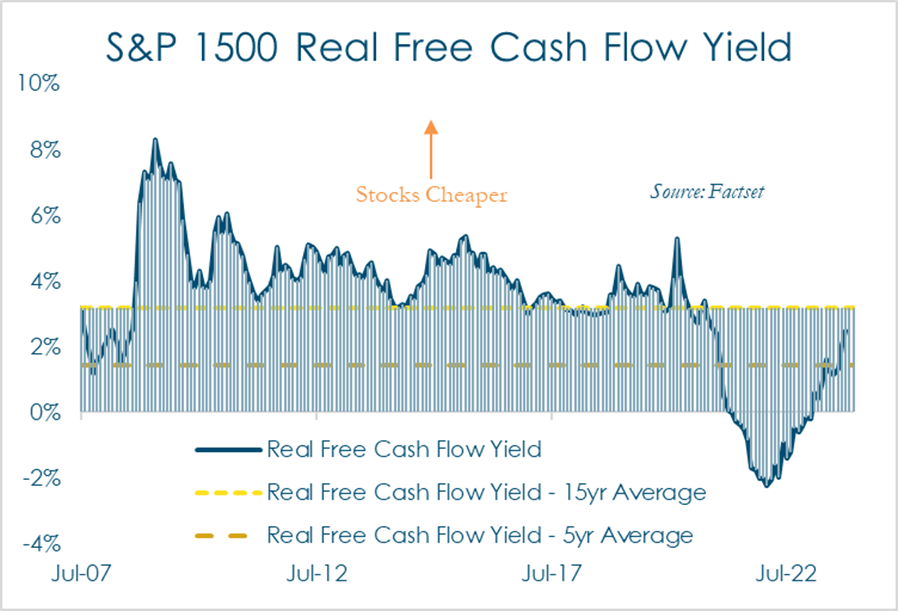

However, as readers of our Review will recall, we prefer to assess equity valuations using an inflation-adjusted cash flow valuation metric, and by this measure, stocks are increasingly cheap, approaching their 15-year average. This is explained by the fact that while earnings may be flat, free cash flow is rising at a similar pace to the rise in stock prices, at the same time inflation is falling, so inflation-adjusted free cash flow yields are improving.

However, as readers of our Review will recall, we prefer to assess equity valuations using an inflation-adjusted cash flow valuation metric, and by this measure, stocks are increasingly cheap, approaching their 15-year average. This is explained by the fact that while earnings may be flat, free cash flow is rising at a similar pace to the rise in stock prices, at the same time inflation is falling, so inflation-adjusted free cash flow yields are improving.

On the other hand, when compared to other asset classes, like US Treasury bonds and Investment Grade Corporate bonds, stocks still appear historically expensive. We expect that as the Federal Reserve lowers its short-term interest rate benchmark in 2024, yields on US Treasuries and Investment Grade corporate bonds will decline, at least for short- and medium-term maturities, and stocks will appear increasingly attractive relative to bonds as the year progresses.

Fixed Income

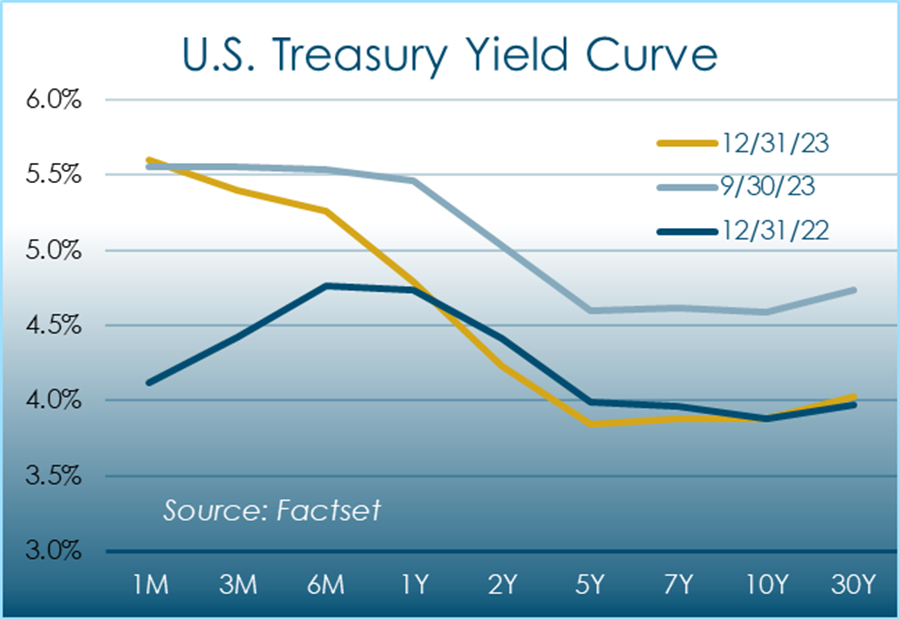

Like stock investors, bond investors began to anticipate the Federal Reserve’s policy shift and bought bonds, driving bond prices up and interest rates, which move inversely to bond prices, down. The move, which occurred during the fourth quarter, took most bond indices from mid-single digit losses to slight gains on the year.

Like stock investors, bond investors began to anticipate the Federal Reserve’s policy shift and bought bonds, driving bond prices up and interest rates, which move inversely to bond prices, down. The move, which occurred during the fourth quarter, took most bond indices from mid-single digit losses to slight gains on the year.

As a result, the yield curve ended with a steep inversion, a phenomenon often portrayed as an indication that a recession at some point in the near- or medium-term is likely. In this case, bond investors are merely anticipating lower interest rates, especially over the next two years, which is how long the Federal Reserve’s rate reduction phase could reasonably last and because of that, we do not view the current inversion as an indication that recession is more likely today than it was 90 days ago.

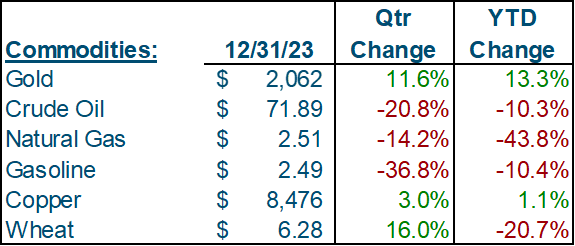

Commodities

Moderating inflation and lower interest rates on U.S. Treasuries provided a supportive backdrop for gold, which rallied significantly during the fourth quarter. Oil on the other hand, suffers from a growing supply surplus, set up by slowing global economic growth, ongoing adoption of EV vehicles, especially in China, and strong oil production in the U.S. Gasoline’s nearly 37% decline is a welcome development for consumers, freeing up more of their incomes for other items.

Moderating inflation and lower interest rates on U.S. Treasuries provided a supportive backdrop for gold, which rallied significantly during the fourth quarter. Oil on the other hand, suffers from a growing supply surplus, set up by slowing global economic growth, ongoing adoption of EV vehicles, especially in China, and strong oil production in the U.S. Gasoline’s nearly 37% decline is a welcome development for consumers, freeing up more of their incomes for other items.

Conclusion

Between the summer’s artificial intelligence frenzy, to the U.S. economy’s surprising resilience, 2023 certainly had a number of surprises for investors, and thankfully, most of them were positive. Virtually every major asset class performed well. We see potential for 2023’s positive economic surprises and financial market performance to continue in 2024, if to a more muted degree.

In 2024 we will be closely watching labor productivity, the linchpin of a goldilocks economy. If employees are more productive each year, even by only a percentage point or two, companies can raise employee compensation slightly faster than inflation, which supports steady, if not spectacular consumer spending, while simultaneously maintaining profit margins at historically high levels, if not expanding them slightly, all without having to raise prices dramatically. Hence, if labor productivity remains modestly positive, the U.S. could experience another phase of productivity-driven growth, without experiencing a debilitating resurgence of inflation, and in the process, get back on track to creating real wealth for the average household.

We expect inflation to fall further, but it may not fall as quickly in 2024 as it did in 2023; there are some key elements of inflation, like health care costs, which are unlikely to fall quickly. Nevertheless, as other items within the inflation measures decline further, the Federal Reserve can slowly lower their benchmark interest rates and release some downward pressure on the economy.

Ordinarily, expectations for a lower Fed Funds rate is accompanied by expectations for a recession. In this case, however, even if economic activity remains solid, as inflation falls further, if the Fed maintains its benchmark rate at its current level, the gap between the Fed’s policy rate and inflation expands; as the gap expands, the Fed’s downward pressure on the economy intensifies.

The degree of downward pressure on the economy is a function, not of the absolute level of the Fed’s benchmark rate, but rather, of the difference between the Fed’s benchmark rate and inflation. If inflation falls, and the Fed maintains its current policy rate, it would be allowing its policy to become more restrictive, and in the process, exacerbating the potential risk of a recession. Certainly, there are some risks to this outlook, and a recession is still a possibility, but as inflation continues to fall and the Fed relaxes its policy stance, the risk of recession recedes.

Against this backdrop, we view bonds favorably since bond prices rise as interest rates fall. We also view stocks favorably, with two caveats; first, returns in 2024 are unlikely to rival those of 2023, and second, last year’s winners are unlikely to be this year’s winners. Investors should temper their expectations for returns, remain disciplined and vigilant, and expect that 2024 will have surprises, just as 2023 did.